When Joe Met Jimmy

Joe Biden was first elected to public office in 1970, the same year that Jimmy Carter was elected governor of Georgia. Two years later in 1972, Biden was elected as a senator from Delaware, and four years after that in 1976, Carter was elected to the presidency with Biden as a worker bee on his behalf.

So, during the late 1970s, Biden served in the Senate while Carter was in the White House. Then in 1980, when Carter was running for re-election, Biden appeared at the Democratic National Convention praising Carter on national television.

In other words, Biden should remember well what life was like during the Carter administration. And he should also remember that Carter went down in a landslide defeat in 1980, losing 41 of 50 states—including Biden’s Delaware—to Ronald Reagan.

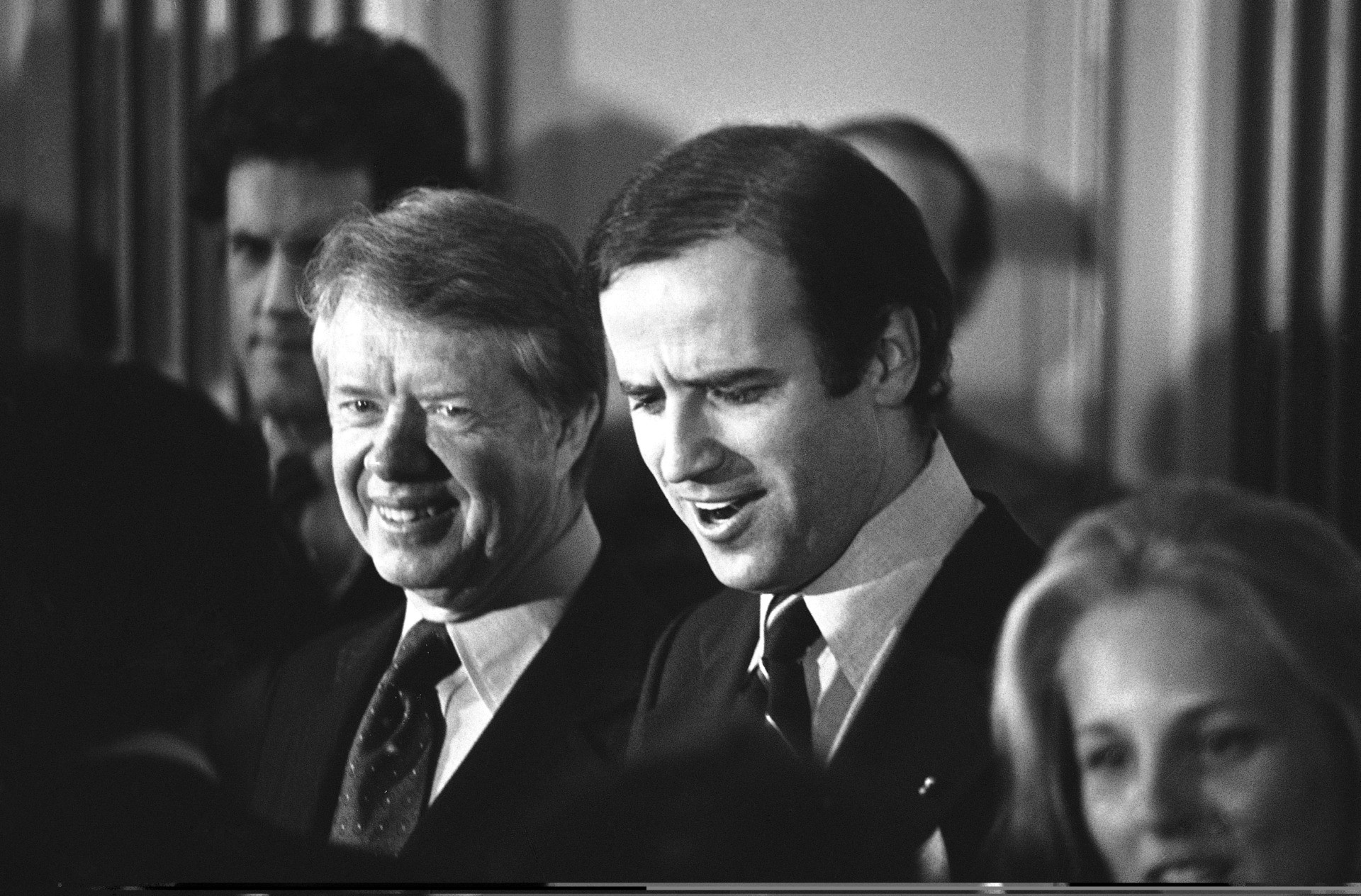

President Jimmy Carter and Sen. Joe Biden greet Biden supporters at a $1,000-a-couple fundraising reception in Wilmington, Delaware, on February 20, 1978. Biden was the first U.S. senator to endorse Carter’s presidential candidacy in 1976. (AP Photo)

Given President Carter’s miserable experience, one might expect that President Biden would be cautious about doing anything that would harken back to the Carter days.

Yet curiously, Biden’s policies are echoing Carter’s in what’s typically the most important issue-area for any president: economic policy. As we shall see, Carter’s policies were not a success—they were, in fact, a disaster—and yet there goes Biden, following down Carter’s path. So if Biden remembers the 1970s, what could he be thinking, re-enacting 70s-type policies?

Perhaps he’s thinking that not that many Americans remember the 1970s—and he’s right about that. In fact, about two thirds of Americans alive today are under the age of 50, which means that they have little or no memory of the larger events of that decade.

Thus we can see: Americans are at risk of finding themselves in the mental trap described by the philosopher George Santayana: “Those who cannot remember the past are condemned to repeat it.” The only escape from this trap, of course, is that we all learn about the past.

So perhaps those of us who do remember the 1970s can offer a refresher on its economic history. Or better yet, a been-there-done-that warning about failed economic policies. Here goes:

The predominant economic school of thought at the beginning of the 1970s was Keynesianism. John Maynard Keynes (1883-1946) believed that the critical variable to economic growth was the maintenance of aggregate demand—that is, the overall willingness of the population to spend money. Yet, of course, people couldn’t spend money unless they had money. So if they lacked money, the government should, Keynes said, print money or borrow money and give it to people who would then spend it, thereby stimulating the economy. Presto! Aggregate demand is maintained, the economy reaches its optimum output, and people are happy. That at least was the theory.

Economist N. Gregory Mankiw, author of a standard economics textbook in the 1990s, explains:

It was the administration of President John F. Kennedy [1961-1963] that first used fiscal policy with the intent of manipulating aggregate demand to move the economy toward its potential output. Kennedy’s willingness to embrace Keynes’s ideas changed the nation’s approach to fiscal policy for the next two decades.

Yet there was a bad side effect from too much pumping up of demand: inflation. That is, if too much demand, or money, is chasing too few goods, then the prices of those goods are bid up. Mankiw further details the impact of the wastrel aggregate-demand policy of the 1960s:

But the inflation that came with it, together with other problems, would create real difficulties for the economy and for macroeconomic policy in the 1970s.

Yes, in the 1970s America suffered a hangover from the spending spree of the previous decade. In the 60s, free-spending policies—most obviously President Lyndon Johnson’s decision to fight the War in Vietnam and the War on Poverty at the same time—caused more than a tripling of the annual change in the Consumer Price Index, from 1.7 percent in 1960 to 5.5 percent in 1969.

That was indeed long ago and far away. In 1969, even after a decade of rising prices, the price of a first-class postage stamp was just six cents, a gallon of gasoline was 36 cents, and the median home price was a little more than $23,000.

Then came the 1970s and real inflation. In the years of that decade, the inflation rate was never lower than 3.2 percent, and it reached as high as 11.3 percent; the average rate was a stiff 7.1 percent. Not surprisingly, consumers—especially those on fixed or limited incomes—were alarmed and angry. And consumers, of course, are also voters. We can add that in 1980, the last year of Jimmy Carter’s presidency, the inflation rate soared to 13.5 percent.

Such inflation was unacceptable, even if it wasn’t so easy to overcome. During the ’70s, three presidents of both parties—Republicans Richard Nixon and Gerald Ford and Democrat Jimmy Carter—struggled to combat inflation; they tried everything from imposing price controls, to wearing lapel buttons, to delivering “malaise” speeches, and yet nothing worked.

To make matters worse, at the same time, the unemployment rate was rising: from 3.9 percent in January 1970, to a peak of nine percent in May 1975, to a still-too-high six percent at the end of 1979.

Most economists were puzzled by this unfortunate concatenation of events, rising prices and rising joblessness. Yet if they couldn’t cure the problem, they could at least give it a name. Thus we had a new portmanteau word: “stagflation”—a fusing of “stagnation” and “inflation.”

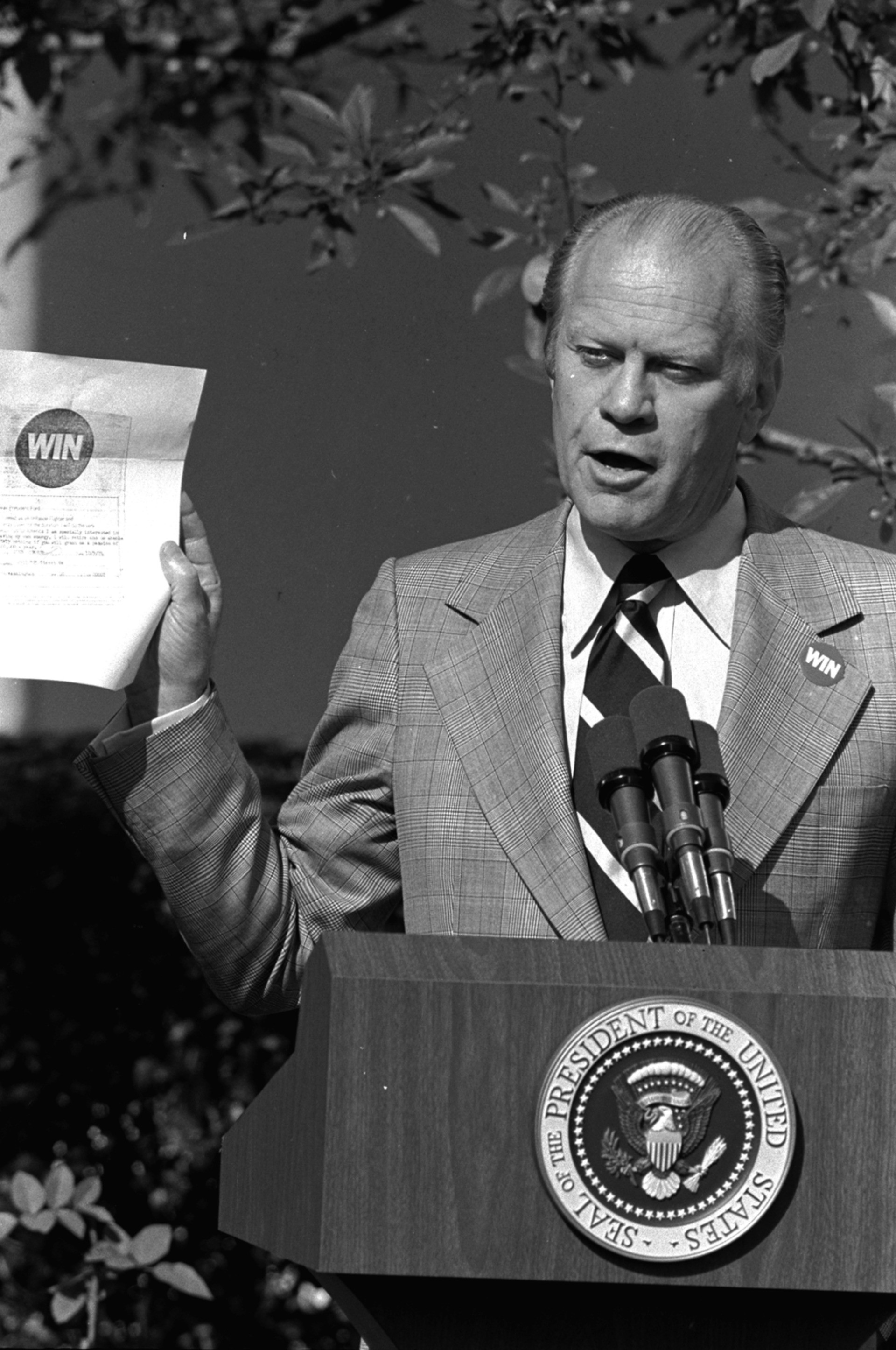

President Gerald Ford, wearing a WIN button on his lapel, holds up a WIN enlistment form which asks citizens to sign up as inflation fighters, during his news conference in the White House Rose Garden on October 9, 1974. WIN stands for Whip Inflation Now. (AP Photo)

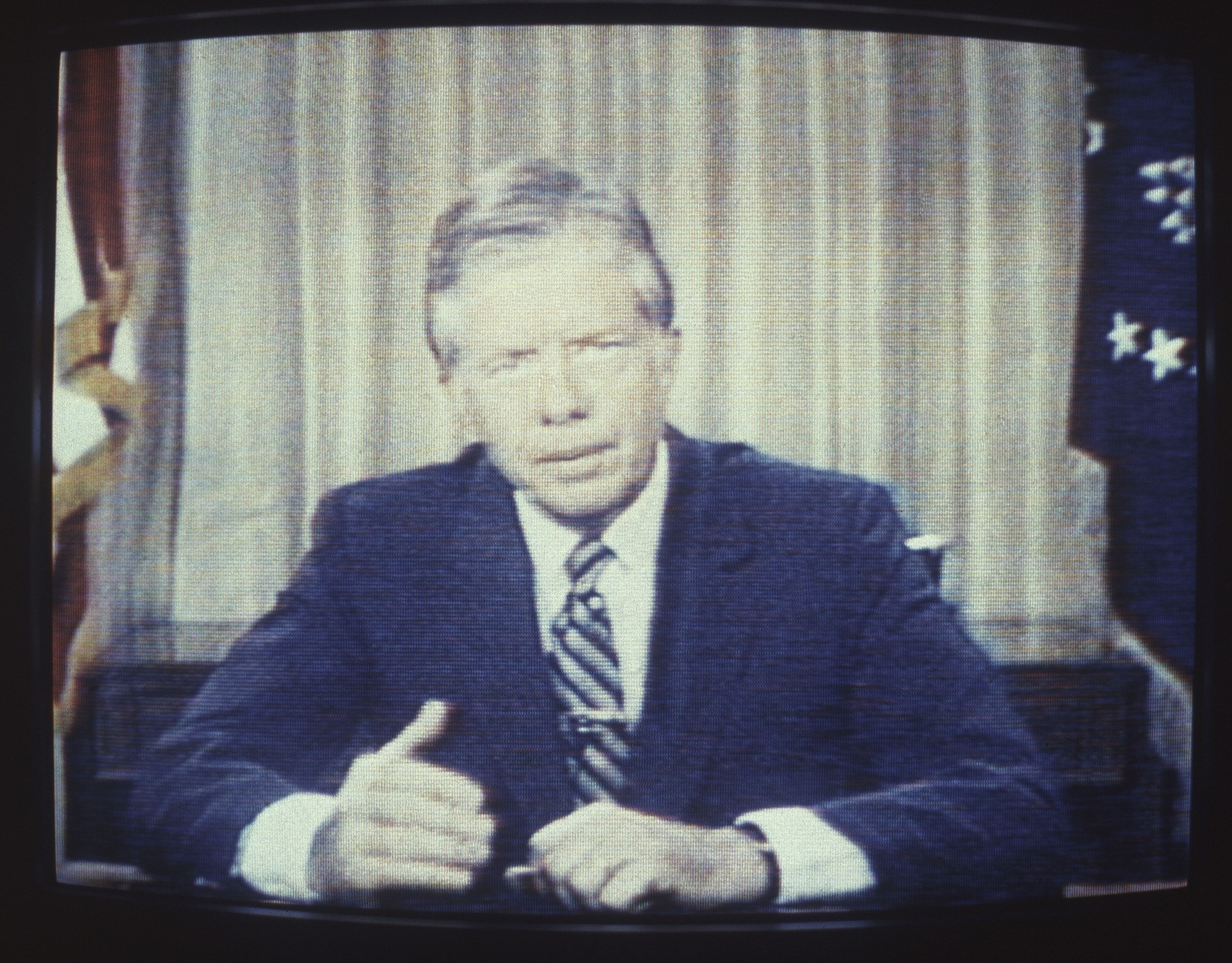

President Jimmy Carter delivers his energy speech, which became known as the “malaise” speech, on television on July 15, 1979. (AP Photo/Dale G. Young)

Demand Side, Meet Supply Side

However, a few rogue economists did step forward with new solutions. One such was Arthur Laffer, whose Laffer Curve showed that high tax rates—the top personal income tax rate in the ’70s was a daunting 70 percent—were stifling productivity and supply. And to Laffer, supply was more important than demand, hence the nickname assigned to Lafferites, “supply siders.” To Laffer and his allies, including Rep. Jack Kemp (R-NY), borrowing or printing money to pump up aggregate demand did not help if supply was being choked by taxes and regulation; in fact, such over-stimulation and under-production proved to be a recipe for still more inflation.

Another economist with a different approach was the late Robert Mundell, who died just on April 4 of this year, at the age of 88. Mundell argued that predictable tight money, not loose money, was vital so that businesses, investors, and governments could make better financial decisions. To Mundell, the whole Keynesian idea of “fine-tuning” aggregate demand was a misnomer; the key was monetary stability.

To put it mildly, the ideas of Laffer and Mundell were viewed as heresy by most of their professional contemporaries. In the words of Mankiw: “Economists did not think in terms of shifts in short-run aggregate supply. Keynesian economics focused on shifts in aggregate demand, not supply.”

Meanwhile, in the White House, Jimmy Carter had to defend his failed economic record. He himself was not a big spender, and yet he defended demand-side economics, even as it dissolved into stagflation. Indeed, during his 1980 re-election campaign, Carter attacked challenger Reagan’s supply-side tax-rate-cutting plan. So what was Carter’s better idea? What was his economic vision for a brighter second term? He didn’t say.

For his part, Reagan was a firm believer in the supply side, which he linked to the basic virtues of hard work, entrepreneurship, and limited government. And in the 1980 election, it was he, not Carter, who prevailed.

After being sworn in as our 40th president, Reagan followed Laffer’s advice and cut tax rates; he also followed Mundell’s idea of tight money.

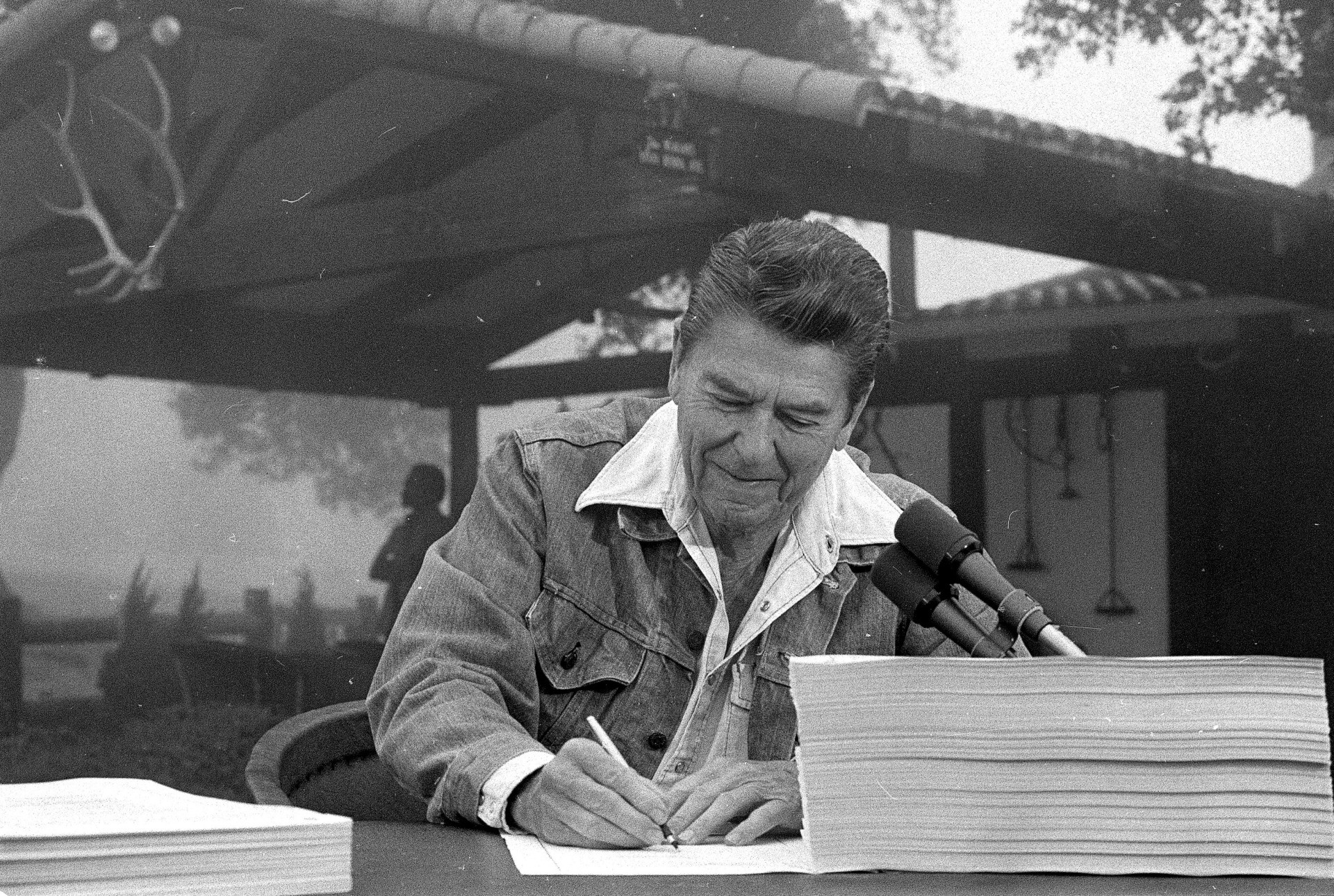

President Ronald Reagan signs the largest tax cut bill in U.S. history at his ranch near Santa Barbara, California, in 1981. (AP Photo/Charles Tasnadi)

There’s no need now to recall the history of Reaganomics, and yet we can observe that the people who knew Reagan best—that is, his fellow Americans living under his leadership—boosted him to a massive re-election in 1984, granting him 525 of their 538 electoral votes.

We can also add that epic rewards came to both Mundell and Laffer. In 1999, Mundell was honored with the Nobel Prize in Economics, and in 2019, Laffer received the Medal of Freedom from President Donald Trump.

But today, Biden is undoing what remains of Reagan’s supply-side legacy; he is shifting his focus back to the demand side. In fact, in contravention of Laffer Curve thinking, Biden has even proposed raising some tax rates. In other words, Biden is on his way back to where he entered into politics—back to the 1970s.

So what does the liberal Main Stream Media think about this shift? The MSM, of course, was never a fan of Reagan, or of his policies. Thus Biden is being greeted with effusive MSM headlines, “The end of Reaganomics,” “Bidenomics beats Reaganomics,” and “Biden’s Huge New Bill Leaves Reaganomics on the Ash Heap of History.” (And of course, to the extent that Trump embraced some of Reagan’s policies, rolling back Reaganomics means rolling back Trumponomics—and the MSM has to love that.)

Most obviously, Biden has returned to the Keynesian prescription of boosting aggregate demand. As The New York Times explained, “The president sees public spending, rather than relying on businesses to turn tax cuts into investment, as the key to competitiveness.”

And since a central tenet of aggregate-demand theory is that the poor have a higher propensity to consume—that is, they are more likely to spend, not save—Biden is most glad to transfer money to the poor. As another New York Times piece declared in its headline, “To Juice the Economy, Biden Bets on the Poor.” As far as the Times is concerned, more spending equals more growth, pure and simple: “Many economists predict that the increase in consumer spending would spur more hiring and business production, helping to lift the economy to its fastest annual growth rate since the mid-1980s.”

So is that really how the economy works? That we can simply spend ourselves rich? The Biden people seem to think so. Once again, journalists and pundits are on board; the MSM abounds with upbeat speculation that Bidenomics could bring about a new “Roaring 20s.”

But what about roaring inflation? After all, the new spending has to be spent somewhere—and so will that pump up aggregate demand to inflationary levels? That’s the concern of Lawrence Summers, a top economic official in the Clinton and Obama administrations. In a February 4 Washington Post op-ed he warned:

There is a chance that macroeconomic stimulus on a scale closer to World War II levels than normal recession levels will set off inflationary pressures of a kind we have not seen in a generation, with consequences for the value of the dollar and financial stability.

The new spending has, after all, been a gusher—a gusher of red ink. According to the Committee for a Responsible Federal Budget, last year’s federal deficit was $3.1 trillion, and this year’s deficit will be $3.4 trillion—although, of course, that number could go up if federal expenditures rise higher than the current level of about $6 trillion.

To look at this spending another way, we can look to the St. Louis Federal Reserve Bank, which calculates that federal spending as a percentage of gross domestic product rose from 20.7 percent in 2019 to 31.3 percent in 2020; yes, that’s the biggest spike in Uncle Sam’s share of GDP since World War II.

And with all that aggregate demand surging into the economy, it’s possible, as Summers suggests, that we could see the sort of rapidly rising prices that blighted the decade of the 1970s—and wrecked Jimmy Carter’s presidency. Indeed, just on April 9, Breitbart News’ financial newsletter took note of the sudden surge in producer prices in March, suggesting a possible annual inflation rate of 4.2 percent. That is, indeed, a 1970s-ish inflation number.

President Joe Biden speaks during an event on the American Jobs Plan in the South Court Auditorium on the White House campus on April 7, 2021, in Washington, DC. (AP Photo/Evan Vucci)

Still, Biden supporters are untroubled; they see inflation as much less of a problem than unemployment. Thus New York magazine hailed Biden’s American Rescue Plan (ARP, the $1.9 trillion Covid bill, which the president signed into law on March 11), as a “paradigm shift.” And specifically addressing the threat of inflation, the author asserted:

With the ARP, the federal government is risking a depreciation in the real value of the economic elite’s bonds and cash holdings for the sake of minimizing involuntary joblessness.

In other words, maybe yes, bonds and cash will depreciate (that’s what happens with inflation). But according to the article, that’s okay, because such depreciation will affect rich people.

Yet in fact, the elite don’t often hold much in the way of bonds or cash; they mostly hold stocks, or own real estate, or other variably priced assets, which often rise with inflation. In addition, of course, the rich tend to pay close attention to their money—and so, of all the income classes, they are the most likely to shift their assets as the need arises.

In other words, if there’s a new bout of inflation, the wealthy will likely be fine—and they’ll still be wealthy, no matter what. In reality, the biggest losers are likely to be those of humbler means, including those on fixed-income pensions and those who keep their funds in a checking account—or under a mattress.

It seems unnecessary to add that there are more voters with middle and low incomes than with high incomes. Which is, to say, by inflating the economy, Biden could be deflating his political standing.

So now we can wonder: If we again suffer from inflation as we had in the 1970s, might the Democrats today suffer another political backlash—as they did in 1980? Surely Biden remembers Reagan giving Carter the boot? Right?

There’s no way to know. And yet we do know, because wise old Santayana told us, Those who cannot remember the past are condemned to repeat it.

COMMENTS

Please let us know if you're having issues with commenting.